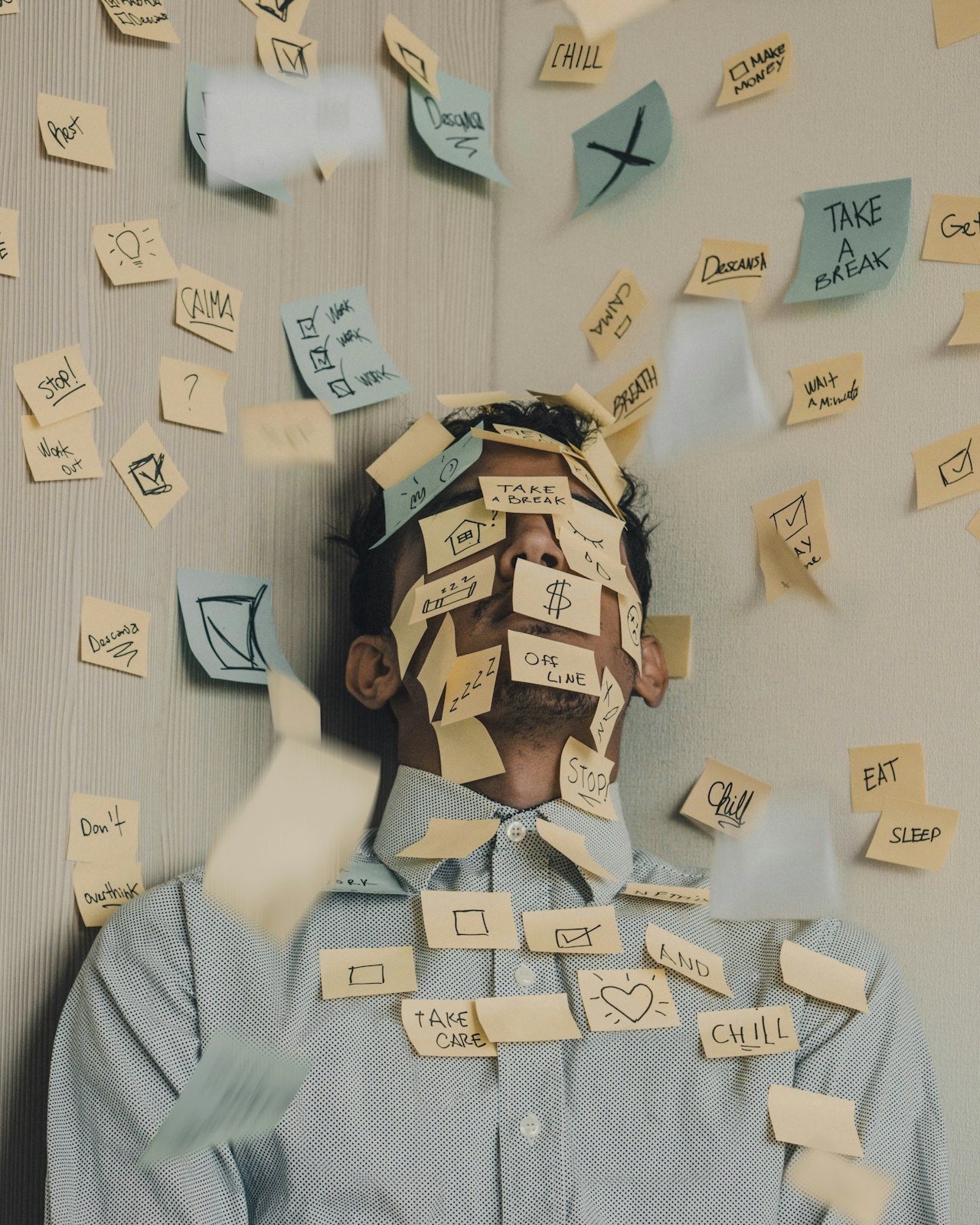

How to manage stress when dealing with home financing

Home Financing Juli Clifford August 17, 2022

Home Financing Juli Clifford August 17, 2022

One excellent way to improve your financial profile is to buy a home of your own. But we won't lie: It's a long and potentially incredibly stressful process, especially when it comes to the dollars and cents of securing a mortgage loan.

One excellent way to improve your financial profile is to buy a home of your own. But we won't lie: It's a long and potentially incredibly stressful process, especially when it comes to the dollars and cents of securing a mortgage loan.

So how do you navigate the stress of the journey in order to reach Destination Homeowner? There's a lot that's within your control to help ease some of that stress and make the whole thing a little bit easier. If you take a few steps upfront to manage the financial details early, you'll thank yourself on moving day.

Get pre-approved for a mortgage

Getting your mortgage loan is arguably the most labor-intensive aspect of buying a home. You'll have to submit documents that show your income and expenses, including tax returns, bank statements, pay stubs, and more. A mortgage pre-approval is much more involved than its lighter cousin, the mortgage pre-qualification.

But a pre-approval will help you understand exactly how your new home will fit into your finances and whether you can even afford the house you're currently touring. Some buyers make the mistake of getting pre-qualified for a mortgage, making an offer on a house they love -- and then discovering once they submit all the paperwork that they can't actually get a loan for that amount.

Sound stressful? It is. Avoid that all-too-common scenario by taking care of the hard part early: Talk to a mortgage lender and get your pre-approval lined up so that when you do find a home that you could call your own, you can place an offer on it then and there without needing to wait for approval from a bank.

Pick the best mortgage for your situation

All mortgages will help you buy a home, but not all mortgages are created equal when it comes to your own personal financial profile.

If you know you're only going to be in your current city for two or three more years before pursuing a career change elsewhere, for example, then maybe a 30-year fixed-rate mortgage is the wrong choice for you. You could build more equity in a shorter period of time with a 15-year mortgage, and an adjustable-rate mortgage might give you a more competitive rate for the time you'll be in the home.

Conversely, if you are planning on digging in and staying for a while, then a 30-year fixed-rate mortgage might be exactly what you need.

If you're a veteran or a first-time homebuyer, then you might be able to access loans from a government-sponsored entity (GSE) like the Federal Housing Administration or Veterans Administration, both of which offer loans that don't require a full 20-percent down payment. And that might mean you can become a homeowner a lot sooner than you thought!

A mortgage broker can walk you through your options and help you choose the mortgage that will work best for your current situation.

Save as much as you can

Even if you're securing a low-down-payment or no-down-payment mortgage, you should still expect some out-of-pocket costs that you'll have to shoulder before you can start paying a mortgage instead of rent.

Depending on the sales contract, buyers will likely have to pay for the appraiser and the inspector to look at the house and (respectively) appraise and inspect it. A seller might request earnest money in order to accept an offer, so buyers will have to provide that. Necessary repairs to the house might be taken on by the buyer in order to expedite the sale, so that's another possible expense to consider. There are closing costs that need to be paid to the title company upon closing, and if a buyer wants to purchase title insurance to protect the sale, that's an additional expense, too. And don't forget about the cost of moving -- you'll need time off work and a truck at minimum, or to hire your own movers. Then once you move in, you might need to pick up some new furniture or other items for your new space.

If you're starting to get the idea that there's no such thing as saving too much before you embark on your home sales journey, then you have the correct impression. Don't let those costs sneak up on you; be aware of them and budget for them so you're not worried about how you're going to get it all done.

Research before you bid

If you've found a home that could be yours and you're ready to make a bid, stop and think before you decide on a number.

You might think that offering the seller's asking price is a perfectly safe move to make (and it might be), but how will you feel when you learn that most sellers in the area are negotiating down from their listing price? (Here's how you'll feel: Like you left several thousand perfectly good dollars on the table that could have been yours.)

A good real estate agent can explain your local market trends and help you come up with a bid that works with your budget and will be seen as serious and competitive by the seller. Agents can show you whether houses in the area have been selling for below or above the asking price and can help you find that sweet spot where both you and the seller are happy with the deal.

Need Help? We're here for you! Reach out - call or text us at: 703-980-0243, or email: [email protected]

new homes

Lot Value in Arlington, VA

new homes

Lot Value Calculator

Home improvement

ROI Comparison Chart - Vienna, VA

Home improvement

Vienna, VA Renovation Estimator

Community

New Construction vs. Established Neighborhoods

Community

Leesburg vs Purcellville

Home improvement

Winter is coming. Well, maybe not immediately, but the season that can be the hardest on our homes is nonetheless approaching.

Home improvement

Out of all the rooms in your home, your kitchen gets the most traffic. Whether you're getting ready to stage and sell your home, or you're unpacking kitchen items into… Read more

Home Financing

Not too long ago in our country's history, talking about making your house "greener" might get you labeled a hippie tree-hugger. But times change, and as gas, electric… Read more

I am committed to guiding you every step of the way—whether you're buying a home, selling a property, or securing a mortgage. Whatever your needs, I've got you covered.

Learn more about Private Exclusive, Compass Coming Soon, & homes not yet on the market!

Juli Clifford of Compass

6849 Old Dominion Dr #400 McLean, VA 22101